Net Positions (Net Longs & Net Shorts) - By LeviathanThis script is an experimental indicator that visualizes the entering and exiting of long and short positions in the market. It also includes other useful tools, such as NL/NS Profile, NL/NS Delta, NL/NS Ratio, Volume Heatmap, Divergence finder, Relative Strength Index of Net Longs and Net Shorts, EMAs and VWMAs and more.

To avoid misinterpretation, it's important to understand some basics. The “real” ratio between net long and net short positions in a given market is always 1:1. A futures contract is an agreement between two parties to buy or sell an underlying asset at an agreed-upon price. Each contract has a long side and a short side, with one party agreeing to buy (long) and the other party agreeing to sell (short) the asset at the agreed-upon price. The long position holder anticipates that the asset's price will rise, while the short position holder expects it to fall. Because every futures contract involves both a buyer and a seller, it is impossible to have more net longs than net shorts or vice versa (in terms of the net value). For every long position opened, there must be a corresponding short position taken by another market participant (and vice versa), thus maintaining the 1:1 ratio between longs and shorts. While there can be an imbalance in the number of traders/accounts holding long and short contracts, the net value of positions held on each side remains 1 to 1.

Open Interest (OI) is a metric that tracks the number of open (unsettled) contracts in a given market. For example, Open Interest of 100 BTC means that there are currently 100 BTC worth of longs and 100 BTC worth of shorts open in the market. There may be more traders on one side holding smaller positions, and fewer traders on the other side holding larger positions, but the net value of positions on one side is equal to the net value of positions on the other side → 100 BTC in longs and 100 BTC in shorts (1:1). Consider a scenario in which a trader decides to open a long position for 1 BTC at a price of HKEX:30 ,000. For this long order to be executed, a counterparty must take the opposite side of the contract by placing an order to short 1 BTC at the same price of HKEX:30 ,000. When both the long and short orders are matched and executed, the open interest increases by 1 BTC, reflecting the addition of this new contract to the market.

Changes in Open Interest essentially tell us 3 things:

- OI Increase - new positions entered the market (both longs and shorts!)

- OI Decrease - positions exited the market (both longs and shorts!)

- OI Flat - no change in open positions due to low activity or simply lots of transfers of contracts

However, different concepts can be used to analyze sentiment, aggressiveness, and activity in the market by analyzing data such as Open Interest, price, volume, etc. This indicator combines Open Interest data and price action to simplify the visualization of positions entering and exiting the market. It is based on the following concept:

Increase in Open Interest + Increase in price = Longs Opening

Decrease in Open Interest + Decrease in price = Longs Closing

Increase in Open Interest + Decrease in price = Shorts Opening

Decrease in Open Interest + Increase in price = Shorts Closing

When "Longs Opening" occurs, the OI Delta value is added to the running total of Net Longs, and when "Longs Closing" occurs, the OI Delta value is subtracted from the running total of Net Longs.

When "Shorts Opening" occurs, the OI Delta value is added to the running total of Net Shorts, and when "Shorts Closing" occurs, the OI Delta value is subtracted from the running total of Net Shorts.

To summarize:

Net Longs: Cumulative value of Longs Opening and Longs Closing (LO - LC)

Net Shorts: Cumulative value of Shorts Opening and Shorts Closing (SO - SC)

Net Delta: Net Longs - Net Shorts

Net Ratio: Net Longs / Net Shorts

This is the fundamental logic of how this script functions, but it also includes several other tools and options. Here is an overview of the settings:

Type:

- Net Positions (display values of Net Longs, Net Shorts, Net Delta, Net Ratio as described above)

- Relative Strength (display Net Longs, Net Shorts, Net Delta, Net Ratio in the form of a momentum oscillator that measures the speed and change of movements. Same logic as RSI for price)

Display as:

- Candles (display the data in the form of candlesticks)

- Lines (display the data in the form of candlesticks)

- Columns (display the data in the form of columns)

Cumulation:

- Visible Range (data is cumulated from the first visible bar on your chart)

- Full Data (data is cumulated from the beginning)

Quoted in:

- Base Currency (all data is presented in the pair’s base currency eg. BTC)

- Quote Currency (all data is presented in the pair’s quote currency eg USDT)

OI Sources

- Pick the sources from where the data is collected (if available).

Net Positions:

- NET LONGS (show/hide Net Longs plot, choose candle colors, choose line color)

- NET SHORTS (show/hide Net Shorts plot, choose candle colors, choose line color)

- NET DELTA (show/hide Net Delta plot, choose candle colors, choose line color)

- NET RATIO (show/hide Net Ratio plot, choose candle colors, choose line color)

Moving Averages:

- Type (choose between EMA and Volume Weighted Moving Average)

- NET LONGS (show/hide NL moving average plot, choose length, choose color)

- NET SHORTS (show/hide NS moving average plot, choose length, choose color)

- NET DELTA (show/hide ND moving average plot, choose length, choose color)

- NET RATIO (show/hide NR moving average plot, choose length, choose color)

Profile:

- Profile Data (choose the source data of the profile)

- Value Area % (set the percentage width of profile’s value area)

- Positions (set the position of the profile to left or right of the visible range)

- Node Size (set the relative size of nodes to make them appear smaller or larger)

- Rows (select the amount of rows displayed by the profile to control granularity)

- POC (show/hide POC- Point Of Control and select its color)

- VA (show/hide VA- Value Area and select its color)

Divergence finder

- Source (choose the source data used by the script to compare it with price pivot points)

- Maximum distance (the maximum distance between two divergent pivot points)

- Lookback Bars Left (the number of bars to the left of the current bar that the function will consider when looking for a pivot point)

- Lookback Bars Right (the number of bars to the right of the current bar that the function will consider when looking for a pivot point)

Stats:

- Show/Hide the Stats table

- Bars Back (choose the length of data analyzed for stats in number of bars)

- Position (choose the position of the Stats table)

- Select Data you want to display in the Stats table

Additional Settings:

- Volume Heatmap (show/hide volume heatmap and select its color)

- Label Offset (select how much the plot label is shifted to the right

- Position Relative Strength Length (select the length used in the calculation)

- Value Label (show/hide OI Delta values when candles are displayed)

- Plot Labels (show/hide the labels next to the plot)

- Wicks (show/hide wick when candles are displayed)

Code used for generating profiles is taken from @KioseffTrading's "Profile Any Indicator" script (used with author's permission)

Search in scripts for "relative strength"

On-Chart QQE of RSI on Variety MA [Loxx]On-Chart QQE of RSI on Variety MA (Quantitative Qualitative Estimation) is usually calculated using RSI. This version is uses an RSI of a Moving Average instead. The results are completely different than the original QQE. Also, this version is drawn directly on chart. There are four types of signals.

What is QQE?

Quantitative Qualitative Estimation (QQE) is a technical analysis indicator used to identify trends and trading opportunities in financial markets. It is based on a combination of two popular technical analysis indicators - the Relative Strength Index (RSI) and Moving Averages (MA).

The QQE indicator uses a smoothed RSI to determine the trend direction, and a moving average of the smoothed RSI to identify potential trend changes. The indicator then plots a series of bands above and below the moving average to indicate overbought and oversold conditions in the market.

The QQE indicator is designed to provide traders with a reliable signal that confirms the strength of a trend or indicates a possible trend reversal. It is particularly useful for traders who are looking to trade in markets that are trending strongly, but also want to identify when a trend is losing momentum or reversing.

Traders can use QQE in a number of different ways, including as a confirmation tool for other indicators or as a standalone indicator. For example, when used in conjunction with other technical analysis tools like support and resistance levels, the QQE indicator can help traders identify key entry and exit points for their trades.

One of the main advantages of the QQE indicator is that it is designed to be more reliable than other indicators that can generate false signals. By smoothing out the price action, the QQE indicator can provide traders with more accurate and reliable signals, which can help them make more profitable trading decisions.

In conclusion, QQE is a popular technical analysis indicator that traders use to identify trends and trading opportunities in financial markets. It combines the RSI and moving average indicators and is designed to provide traders with reliable signals that confirm the strength of a trend or indicate a possible trend reversal.

What is RSI?

RSI stands for Relative Strength Index . It is a technical indicator used to measure the strength or weakness of a financial instrument's price action.

The RSI is calculated based on the price movement of an asset over a specified period of time, typically 14 days, and is expressed on a scale of 0 to 100. The RSI is considered overbought when it is above 70 and oversold when it is below 30.

Traders and investors use the RSI to identify potential buy and sell signals. When the RSI indicates that an asset is oversold, it may be considered a buying opportunity, while an overbought RSI may signal that it is time to sell or take profits.

It's important to note that the RSI should not be used in isolation and should be used in conjunction with other technical and fundamental analysis tools to make informed trading decisions.

This indicator makes use of the following libraries:

Loxx's Moving Averages

Loxx's Expanded Source Types

Extras

Alerts

Signals

Signal Types

Change on Levels

Change on Slope

Change on Zero

Change on Original

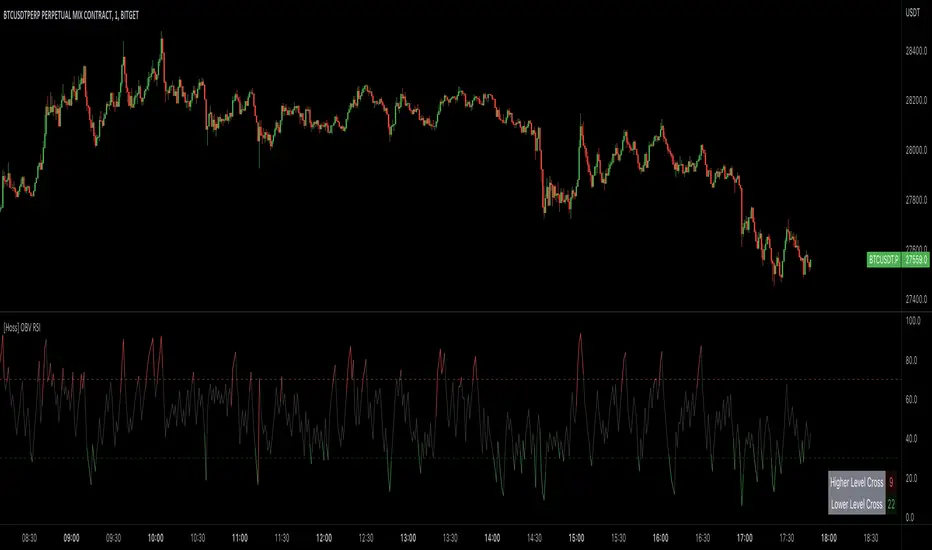

[Hoss] OBV RSIThe OBV ( On Balance Volume ) RSI ( Relative Strength Index ) indicator is an innovative tool that combines the power of OBV and RSI to provide traders with a comprehensive view of the market's momentum and volume dynamics. This combination enables users to make better-informed trading decisions by analyzing the relationship between price, volume , and relative strength .

The script starts by calculating the On Balance Volume , which is a cumulative volume-based indicator that measures buying and selling pressure. The OBV increases when the closing price is higher than the previous closing price and decreases when the closing price is lower than the previous closing price. This helps traders identify potential price trend reversals based on volume accumulation or distribution.

Next, the script computes the Relative Strength Index ( RSI ) based on the OBV values, offering a unique perspective on the market's momentum through the lens of volume . The RSI is a popular momentum indicator that ranges from 0 to 100 and helps traders identify overbought and oversold conditions. In this script, the user can define the RSI length and the higher and lower levels (default values are 70 and 30, respectively).

A distinctive feature of this OBV RSI indicator is the addition of a monitor that counts the number of times the RSI crosses above the higher level and below the lower level within a user-defined lookback period. This monitor is displayed as a table in the bottom right corner of the chart and can be enabled or disabled through an input option.

The cross count monitor provides valuable insights into the historical frequency of RSI crossings, helping traders to identify potential trading opportunities based on historical price behavior around these levels.

swami_rsi

Description:

As in the practices, most traders find it hard to set the proper lookback period of the indicator to be used. SwamiCharts offers a comprehensive way to visualize the indicator used over a range of lookback periods. The SwamiCharts of Relative Strength Index (RSI), was developed by Ehlers - see Cycle Analytics for Traders, chapter 16. The indicator was computed over multiple times of the range of lookback period for the Relative Strength Index (RSI), from the deficient period to the relatively high lookback period i.e. 1 to 48, then plotted as one heatmap.

Features:

In this indicator, the improvement is to utilize the color(dot)rgb() function, which finds to giving a relatively lower time to compute, and follows the original color scheme.

The confirmation level, which assumed of 25

[blackcat] L3 RMI Trading StrategyLevel 3

Background

My view of correct usage of RSI and the relationship between RMI and RSI. A proposed RMI indicator with features is introduced

Descriptions

The Relative Strength Index (RSI) is a technical indicator that many people use. Its focus indicates the strength or weakness of a stock. In the traditional usage of this point, when the RSI is above 50, it is strong, otherwise it is weak. Above 80 is overbought, below 20 is oversold. This is what the textbook says. However, if you follow the principles in this textbook and enter the actual trading, you would lose a lot and win a little! What is the reason for this? When the RSI is greater than 50, that is, a stock enters the strong zone. At this time, the emotions of market may just be brewing, and as a result, you run away and watch others win profit. On the contrary, when RSI<20, that is, a stock enters the weak zone, you buy it. At this time, the effect of losing money is spreading. You just took over the chips that were dumped by the whales. Later, you thought that you had bought at the bottom, but found that you were in half mountainside. According to this cycle, there is a high probability that a phenomenon will occur: if you sell, price will rise, and if you buy, price will fall, who have similar experiences should quickly recall whether their RSI is used in this way. Technical indicators are weapons. It can be either a tool of bull or a sharp blade of bear. Don't learn from dogma and give it away. Trading is a game of people. There is an old saying called “people’s hearts are unpredictable”. Do you really think that there is a tool that can detect the true intentions of people’s hearts 100% of the time?

For the above problems, I suggest that improvements can be made in two aspects (in other words, once the strategy is widely spread, it is only a matter of time before it fails. The market is an adaptive and complex system, as long as it can be fully utilized under the conditions that can be used, it is not easy to use. throw or evolve):

1. RSI usage is the opposite. When a stock has undergone a deep adjustment from a high level, and the RSI has fallen from a high of more than 80 to below 50, it has turned from strong to weak, and cannot be bought in the short term. But when the RSI first moved from a low to a high of 80, it just proved that the stock was in a strong zone. There are funds in the activity, put into the stock pool.

Just wait for RSI to intervene in time when it shrinks and pulls back (before it rises when the main force washes the market). It is emphasized here that the use of RSI should be combined with trading volume, rising volume, and falling volume are all healthy performances. A callback that does not break an important moving average is a confirmed buying point or a second step back on an important moving average is a more certain buying point.

2. The RSI is changed to a more stable and adjustable RMI (Relative Momentum Indicator), which is characterized by an additional momentum parameter, which can not only be very close to the RSI performance, but also adjust the momentum parameter m when the market environment changes to ensure more A good fit for a changing market.

The Relative Momentum Index (RMI) was developed by Roger Altman and described its principles in his article in the February 1993 issue of the journal Technical Analysis of Stocks and Commodities. He developed RMI based on the RSI principle. For example, RSI is calculated from the close to yesterday's close in a period of time compared to the ups and downs, while the RMI is compared from the close to the close of m days ago. Therefore, in principle, when m=1, RSI should be equal to RMI. But it is precisely because of the addition of this m parameter that the RMI result may be smoother than the RSI.

Not much more to say, the below picture: when m=1, RMI and RSI overlap, and the result is the same.

The Shanghai 50 Index is from TradingView (m=1)

The Shanghai 50 Index is from TradingView (m=3)

The Shanghai 50 Index is from TradingView (m=5)

For this indicator function, I also make a brief introduction:

1. 50 is the strength line (white), do not operate offline, pay attention online. 80 is the warning line (yellow), indicating that the stock has entered a strong area; 90 is the lightening line (orange), once it is greater than 90 and a sell K-line pattern appears, the position will be lightened; the 95 clearing line (red) means that selling is at a climax. This is seen from the daily and weekly cycles, and small cycles may not be suitable.

2. The purple band indicates that the momentum is sufficient to hold a position, and the green band indicates that the momentum is insufficient and the position is short.

3. Divide the RMI into 7, 14, and 21 cycles. When the golden fork appears in the two resonances, a golden fork will appear to prompt you to buy, and when the two periods of resonance have a dead fork, a purple fork will appear to prompt you to sell.

4. Add top-bottom divergence judgment algorithm. Top_Div red label indicates top divergence; Bot_Div green label indicates bottom divergence. These signals are only for auxiliary judgment and are not 100% accurate.

5. This indicator needs to be combined with VOL energy, K-line shape and moving average for comprehensive judgment. It is still in its infancy, and open source is published in the TradingView community. A more complete advanced version is also considered for subsequent release (because the K-line pattern recognition algorithm is still being perfected).

Remarks

Feedbacks are appreciated.

Relative Index StrengthThis script shows relative strength of custom stock compared to Index. It is helpful in detecting how strongly a stock is performing when compared to an Index.

When the index is falling but the custom stock is rising, indicator shows this in red with its relative strength compared to index, indicating the stock is moving strongly against market trend.

When the index and the custom stock are moving in same direction, indicator remains neutral, indicating the stock is aligned with the market trend.

Adaptivity: Measures of Dominant Cycles and Price Trend [Loxx]Adaptivity: Measures of Dominant Cycles and Price Trend is an indicator that outputs adaptive lengths using various methods for dominant cycle and price trend timeframe adaptivity. While the information output from this indicator might be useful for the average trader in one off circumstances, this indicator is really meant for those need a quick comparison of dynamic length outputs who wish to fine turn algorithms and/or create adaptive indicators.

This indicator compares adaptive output lengths of all publicly known adaptive measures. Additional adaptive measures will be added as they are discovered and made public.

The first released of this indicator includes 6 measures. An additional three measures will be added with updates. Please check back regularly for new measures.

Ehers:

Autocorrelation Periodogram

Band-pass

Instantaneous Cycle

Hilbert Transformer

Dual Differentiator

Phase Accumulation (future release)

Homodyne (future release)

Jurik:

Composite Fractal Behavior (CFB)

Adam White:

Veritical Horizontal Filter (VHF) (future release)

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman's adaptive moving average (KAMA) and Tushar Chande's variable index dynamic average (VIDYA) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index (RSI), commodity channel index (CCI), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

What is this Hilbert Transformer?

An analytic signal allows for time-variable parameters and is a generalization of the phasor concept, which is restricted to time-invariant amplitude, phase, and frequency. The analytic representation of a real-valued function or signal facilitates many mathematical manipulations of the signal. For example, computing the phase of a signal or the power in the wave is much simpler using analytic signals.

The Hilbert transformer is the technique to create an analytic signal from a real one. The conventional Hilbert transformer is theoretically an infinite-length FIR filter. Even when the filter length is truncated to a useful but finite length, the induced lag is far too large to make the transformer useful for trading.

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, pages 186-187:

"I want to emphasize that the only reason for including this section is for completeness. Unless you are interested in research, I suggest you skip this section entirely. To further emphasize my point, do not use the code for trading. A vastly superior approach to compute the dominant cycle in the price data is the autocorrelation periodogram. The code is included because the reader may be able to capitalize on the algorithms in a way that I do not see. All the algorithms encapsulated in the code operate reasonably well on theoretical waveforms that have no noise component. My conjecture at this time is that the sample-to-sample noise simply swamps the computation of the rate change of phase, and therefore the resulting calculations to find the dominant cycle are basically worthless.The imaginary component of the Hilbert transformer cannot be smoothed as was done in the Hilbert transformer indicator because the smoothing destroys the orthogonality of the imaginary component."

What is the Dual Differentiator, a subset of Hilbert Transformer?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 187:

"The first algorithm to compute the dominant cycle is called the dual differentiator. In this case, the phase angle is computed from the analytic signal as the arctangent of the ratio of the imaginary component to the real component. Further, the angular frequency is defined as the rate change of phase. We can use these facts to derive the cycle period."

What is the Phase Accumulation, a subset of Hilbert Transformer?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 189:

"The next algorithm to compute the dominant cycle is the phase accumulation method. The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle's worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio."

What is the Homodyne, a subset of Hilbert Transformer?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 192:

"The third algorithm for computing the dominant cycle is the homodyne approach. Homodyne means the signal is multiplied by itself. More precisely, we want to multiply the signal of the current bar with the complex value of the signal one bar ago. The complex conjugate is, by definition, a complex number whose sign of the imaginary component has been reversed."

What is the Instantaneous Cycle?

The Instantaneous Cycle Period Measurement was authored by John Ehlers; it is built upon his Hilbert Transform Indicator.

From his Ehlers' book Cybernetic Analysis for Stocks and Futures: Cutting-Edge DSP Technology to Improve Your Trading by John F. Ehlers, 2004, page 107:

"It is obvious that cycles exist in the market. They can be found on any chart by the most casual observer. What is not so clear is how to identify those cycles in real time and how to take advantage of their existence. When Welles Wilder first introduced the relative strength index (rsi), I was curious as to why he selected 14 bars as the basis of his calculations. I reasoned that if i knew the correct market conditions, then i could make indicators such as the rsi adaptive to those conditions. Cycles were the answer. I knew cycles could be measured. Once i had the cyclic measurement, a host of automatically adaptive indicators could follow.

Measurement of market cycles is not easy. The signal-to-noise ratio is often very low, making measurement difficult even using a good measurement technique. Additionally, the measurements theoretically involve simultaneously solving a triple infinity of parameter values. The parameters required for the general solutions were frequency, amplitude, and phase. Some standard engineering tools, like fast fourier transforms (ffs), are simply not appropriate for measuring market cycles because ffts cannot simultaneously meet the stationarity constraints and produce results with reasonable resolution. Therefore i introduced maximum entropy spectral analysis (mesa) for the measurement of market cycles. This approach, originally developed to interpret seismographic information for oil exploration, produces high-resolution outputs with an exceptionally short amount of information. A short data length improves the probability of having nearly stationary data. Stationary data means that frequency and amplitude are constant over the length of the data. I noticed over the years that the cycles were ephemeral. Their periods would be continuously increasing and decreasing. Their amplitudes also were changing, giving variable signal-to-noise ratio conditions. Although all this is going on with the cyclic components, the enduring characteristic is that generally only one tradable cycle at a time is present for the data set being used. I prefer the term dominant cycle to denote that one component. The assumption that there is only one cycle in the data collapses the difficulty of the measurement process dramatically."

What is the Band-pass Cycle?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 47:

"Perhaps the least appreciated and most underutilized filter in technical analysis is the band-pass filter. The band-pass filter simultaneously diminishes the amplitude at low frequencies, qualifying it as a detrender, and diminishes the amplitude at high frequencies, qualifying it as a data smoother. It passes only those frequency components from input to output in which the trader is interested. The filtering produced by a band-pass filter is superior because the rejection in the stop bands is related to its bandwidth. The degree of rejection of undesired frequency components is called selectivity. The band-stop filter is the dual of the band-pass filter. It rejects a band of frequency components as a notch at the output and passes all other frequency components virtually unattenuated. Since the bandwidth of the deep rejection in the notch is relatively narrow and since the spectrum of market cycles is relatively broad due to systemic noise, the band-stop filter has little application in trading."

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 59:

"The band-pass filter can be used as a relatively simple measurement of the dominant cycle. A cycle is complete when the waveform crosses zero two times from the last zero crossing. Therefore, each successive zero crossing of the indicator marks a half cycle period. We can establish the dominant cycle period as twice the spacing between successive zero crossings."

What is Composite Fractal Behavior (CFB)?

All around you mechanisms adjust themselves to their environment. From simple thermostats that react to air temperature to computer chips in modern cars that respond to changes in engine temperature, r.p.m.'s, torque, and throttle position. It was only a matter of time before fast desktop computers applied the mathematics of self-adjustment to systems that trade the financial markets.

Unlike basic systems with fixed formulas, an adaptive system adjusts its own equations. For example, start with a basic channel breakout system that uses the highest closing price of the last N bars as a threshold for detecting breakouts on the up side. An adaptive and improved version of this system would adjust N according to market conditions, such as momentum, price volatility or acceleration.

Since many systems are based directly or indirectly on cycles, another useful measure of market condition is the periodic length of a price chart's dominant cycle, (DC), that cycle with the greatest influence on price action.

The utility of this new DC measure was noted by author Murray Ruggiero in the January '96 issue of Futures Magazine. In it. Mr. Ruggiero used it to adaptive adjust the value of N in a channel breakout system. He then simulated trading 15 years of D-Mark futures in order to compare its performance to a similar system that had a fixed optimal value of N. The adaptive version produced 20% more profit!

This DC index utilized the popular MESA algorithm (a formulation by John Ehlers adapted from Burg's maximum entropy algorithm, MEM). Unfortunately, the DC approach is problematic when the market has no real dominant cycle momentum, because the mathematics will produce a value whether or not one actually exists! Therefore, we developed a proprietary indicator that does not presuppose the presence of market cycles. It's called CFB (Composite Fractal Behavior) and it works well whether or not the market is cyclic.

CFB examines price action for a particular fractal pattern, categorizes them by size, and then outputs a composite fractal size index. This index is smooth, timely and accurate

Essentially, CFB reveals the length of the market's trending action time frame. Long trending activity produces a large CFB index and short choppy action produces a small index value. Investors have found many applications for CFB which involve scaling other existing technical indicators adaptively, on a bar-to-bar basis.

What is VHF Adaptive Cycle?

Vertical Horizontal Filter (VHF) was created by Adam White to identify trending and ranging markets. VHF measures the level of trend activity, similar to ADX DI. Vertical Horizontal Filter does not, itself, generate trading signals, but determines whether signals are taken from trend or momentum indicators. Using this trend information, one is then able to derive an average cycle length.

KINSKI Multi Trend OscillatorThe Multi Trend Oscillator is a tool that combines the ratings of several indicators to facilitate the search for profitable trades. I was inspired by the excellent indicator "Technical Ratings" from Team TradingView to create an alternative with a technically new approach. Therefore, it is not a modified copy of the original, but newly conceived and implemented.

The recommendations of the indicator are based on the calculated ratings from the different indicators included in it. The special thing here is that all settings for the individual indicators can be changed according to your own needs and displayed as a histogram and MA line. This provides an excellent visual control of your own settings. Alarms are also triggered.

Criteria for determining the rating

Relative Strength Index (RSI)

Buy - Crossover oversold level and indicator < oversold level and rising

Sell - Crossunder oversold level and indicator >= oversold level and falling

Neutral - neither Buy nor Sell

Relative Strength Index (RSI) Laguerre

Buy - Crossover Oversold Level and Indicator < Oversold Level and rising

Sell - Crossunder oversold level and indicator >= oversold level and falling

Neutral - neither Buy nor Sell

Noise free Relative Strength Index (RSX)

Buy - Crossover Oversold Level and Indicator < Oversold Level and rising

Sell - Crossunder oversold level and indicator >= oversold level and falling

Neutral - neither Buy nor Sell

Money Flow Index (MFI)

Buy - Crossover Oversold Level and Indicator < Oversold Level and rising

Sell - Crossunder oversold level and indicator >= oversold level and falling

Neutral - neither Buy nor Sell

Commodity Channel Index (CCI)

Buy - Crossover Oversold Level and Indicator < Oversold Level and rising

Sell - Crossunder oversold level and indicator >= oversold level and falling

Neutral - neither Buy nor Sell

Moving Average Convergence/Divergence (MACD)

Buy - values of the main line > values of the signal line and rising

Sell - values of the main line < values of the signal line and falling

Neutral - neither Buy nor Sell

Klinger

Buy - indicator >= 0 and rising

Sell - indicator < 0 and falling

Neutral - neither Buy nor Sell

Average Directional Index (ADX)

Buy - indicator > 20 and +DI line crosses over the -DI line and rising

Sell - indicator > 20 and +DI line crosses below the -DI line and falling

Neutral - neither Buy nor Sell

Awesome Oscillator

Buy - Crossover 0 and values are greater than 0, or exceed the zero line

Sell - Crossunder 0 and values are lower than 0, or fall below the zero line

Neutral - neither Buy nor Sell

Ultimate Oscillator

Buy - Crossover oversold level and indicator < oversold level and rising

Sell - Crossunder oversold level and indicator >= oversold level and falling

Neutral - neither Buy nor Sell

Williams Percent Range

Buy - Crossover Oversold Level and Indicator < Oversold Level and rising

Sell - Crossunder Oversold Level and Indicator >= Oversold Level and falling

Neutral - neither Buy nor Sell

Momentum

Buy - Crossover 0 and indicator levels rising

Sell - Crossunder 0 and indicator values falling

Neutral - neither Buy nor Sell

Total Ratings

The numerical value of the rating "Sell" is 0, "Neutral" is 0 and "Buy" is 1. The total rating is calculated as the average of the ratings of the individual indicators and are determined according to the following criteria:

MaxCount = 12 (depending on whether other oscillators are added).

CompareSellStrong = MaxCount * 0.3

CompareMid = MaxCount * 0.5

CompareBuyStrong = MaxCount * 0.7

value <= CompareSellStrong - Strong Sell

value < CompareMid and value > CompareSellStrong - Sell

value == 6 - Neutral

value > CompareMid and value < CompareBuyStrong - Buy

value >= CompareBuyStrong - Strong Buy

Understanding the results

The Multi Trend Oscillator is designed so that its values fluctuate between 0 and currently 12 (maximum number of integrated indicators). Its values are displayed as a histogram with green, red and gray bars. The bars are gray when the value of the indicator is at half of the number of indicators used, currently 12. Increasingly saturated green bars indicate increasing values above 6, and increasingly saturated red bars indicate increasingly decreasing values below 6.

The table at the end of the histogram shows details (can be activated in the settings) about the overall rating and the individual indicators. Its color is determined by the rating value: gray for neutral, green for buy or strong buy, red for sell or strong sell.

The following alarms are triggered:

Multi Trend Oscillator: Sell

Multi Trend Oscillator: Strong Sell

Multi Trend Oscillator: Buy

Multi Trend Oscillator: Strong Buy

Cyclic RSI High Low With Noise Filter█ OVERVIEW

This indicator displays Cyclic Relative Strength Index based on Decoding the Hidden Market Rhythm, Part 1 written by Lars von Thienen.

To determine true or false for Overbought / Oversold are unnecessary, therefore these should be either strong or weak.

Noise for weak Overbought / Oversold can be filtered, especially for smaller timeframe.

█ FEATURES

Display calculated Cyclic Relative Strength Index.

Zigzag high low based on Cyclic Relative Strength Index.

Able to filter noise for high low.

█ LEGENDS

◍ Weak Overbought / Oversold

OB ▼ = Strong Overbought

OS ▲ = Strong Oversold

█ USAGE / TIPS

Recommend to be used for Harmonic Patterns such as XABCD and ABCD.

Condition 1 (XABCD) : When ▼ and ▲ exist side by side, usually this outline XA, while the next two ◍ can be BC.

Condition 2 (ABCD) : When ▼ and ▲ exist side by side, usually this outline AB, while the next one ◍ can be BC, strong ABCD.

Condition 3 (ABCD) : When ▼ or ▲ exist at Point A, the next two ◍ can be Point B and Point C, medium ABCD.

Condition 4 (ABCD) : When ◍ exist at Point a, the next two ◍ can be Point b and Point c, weak ABCD usually used as lower case as abcd.

█ CREDITS

LoneSomeTheBlue

WhenToTrade

pandas_taLibrary "pandas_ta"

Level: 3

Background

Today is the first day of 2022 and happy new year every tradingviewers! May health and wealth go along with you all the time. I use this chance to publish my 1st PINE v5 lib : pandas_ta

This is not a piece of cake like thing, which cost me a lot of time and efforts to build this lib. Beyond 300 versions of this script was iterated in draft.

Function

Library "pandas_ta"

PINE v5 Counterpart of Pandas TA - A Technical Analysis Library in Python 3 at github.com

The Original Pandas Technical Analysis (Pandas TA) is an easy to use library that leverages the Pandas package with more than 130 Indicators and Utility functions and more than 60 TA Lib Candlestick Patterns.

I realized most of indicators except Candlestick Patterns because tradingview built-in Candlestick Patterns are even more powerful!

I use this to verify pandas_ta python version indicators for myself, but I realize that maybe many may need similar lib for pine v5 as well.

Function Brief Descriptions (Pls find details in script comments)

bton --> Binary to number

wcp --> Weighted Closing Price (WCP)

counter --> Condition counter

xbt --> Between

ebsw --> Even Better SineWave (EBSW)

ao --> Awesome Oscillator (AO)

apo --> Absolute Price Oscillator (APO)

xrf --> Dynamic shifted values

bias --> Bias (BIAS)

bop --> Balance of Power (BOP)

brar --> BRAR (BRAR)

cci --> Commodity Channel Index (CCI)

cfo --> Chande Forcast Oscillator (CFO)

cg --> Center of Gravity (CG)

cmo --> Chande Momentum Oscillator (CMO)

coppock --> Coppock Curve (COPC)

cti --> Correlation Trend Indicator (CTI)

dmi --> Directional Movement Index(DMI)

er --> Efficiency Ratio (ER)

eri --> Elder Ray Index (ERI)

fisher --> Fisher Transform (FISHT)

inertia --> Inertia (INERTIA)

kdj --> KDJ (KDJ)

kst --> 'Know Sure Thing' (KST)

macd --> Moving Average Convergence Divergence (MACD)

mom --> Momentum (MOM)

pgo --> Pretty Good Oscillator (PGO)

ppo --> Percentage Price Oscillator (PPO)

psl --> Psychological Line (PSL)

pvo --> Percentage Volume Oscillator (PVO)

qqe --> Quantitative Qualitative Estimation (QQE)

roc --> Rate of Change (ROC)

rsi --> Relative Strength Index (RSI)

rsx --> Relative Strength Xtra (rsx)

rvgi --> Relative Vigor Index (RVGI)

slope --> Slope

smi --> SMI Ergodic Indicator (SMI)

sqz* --> Squeeze (SQZ) * NOTE: code sufferred from very strange error, code was commented.

sqz_pro --> Squeeze PRO(SQZPRO)

xfl --> Condition filter

stc --> Schaff Trend Cycle (STC)

stoch --> Stochastic (STOCH)

stochrsi --> Stochastic RSI (STOCH RSI)

trix --> Trix (TRIX)

tsi --> True Strength Index (TSI)

uo --> Ultimate Oscillator (UO)

willr --> William's Percent R (WILLR)

alma --> Arnaud Legoux Moving Average (ALMA)

xll --> Dynamic rolling lowest values

dema --> Double Exponential Moving Average (DEMA)

ema --> Exponential Moving Average (EMA)

fwma --> Fibonacci's Weighted Moving Average (FWMA)

hilo --> Gann HiLo Activator(HiLo)

hma --> Hull Moving Average (HMA)

hwma --> HWMA (Holt-Winter Moving Average)

ichimoku --> Ichimoku Kinkō Hyō (ichimoku)

jma --> Jurik Moving Average Average (JMA)

kama --> Kaufman's Adaptive Moving Average (KAMA)

linreg --> Linear Regression Moving Average (linreg)

mgcd --> McGinley Dynamic Indicator

rma --> wildeR's Moving Average (RMA)

sinwma --> Sine Weighted Moving Average (SWMA)

ssf --> Ehler's Super Smoother Filter (SSF) © 2013

supertrend --> Supertrend (supertrend)

xsa --> X simple moving average

swma --> Symmetric Weighted Moving Average (SWMA)

t3 --> Tim Tillson's T3 Moving Average (T3)

tema --> Triple Exponential Moving Average (TEMA)

trima --> Triangular Moving Average (TRIMA)

vidya --> Variable Index Dynamic Average (VIDYA)

vwap --> Volume Weighted Average Price (VWAP)

vwma --> Volume Weighted Moving Average (VWMA)

wma --> Weighted Moving Average (WMA)

zlma --> Zero Lag Moving Average (ZLMA)

entropy --> Entropy (ENTP)

kurtosis --> Rolling Kurtosis

skew --> Rolling Skew

xev --> Condition all

zscore --> Rolling Z Score

adx --> Average Directional Movement (ADX)

aroon --> Aroon & Aroon Oscillator (AROON)

chop --> Choppiness Index (CHOP)

xex --> Condition any

cksp --> Chande Kroll Stop (CKSP)

dpo --> Detrend Price Oscillator (DPO)

long_run --> Long Run

psar --> Parabolic Stop and Reverse (psar)

short_run --> Short Run

vhf --> Vertical Horizontal Filter (VHF)

vortex --> Vortex

accbands --> Acceleration Bands (ACCBANDS)

atr --> Average True Range (ATR)

bbands --> Bollinger Bands (BBANDS)

donchian --> Donchian Channels (DC)

kc --> Keltner Channels (KC)

massi --> Mass Index (MASSI)

natr --> Normalized Average True Range (NATR)

pdist --> Price Distance (PDIST)

rvi --> Relative Volatility Index (RVI)

thermo --> Elders Thermometer (THERMO)

ui --> Ulcer Index (UI)

ad --> Accumulation/Distribution (AD)

cmf --> Chaikin Money Flow (CMF)

efi --> Elder's Force Index (EFI)

ecm --> Ease of Movement (EOM)

kvo --> Klinger Volume Oscillator (KVO)

mfi --> Money Flow Index (MFI)

nvi --> Negative Volume Index (NVI)

obv --> On Balance Volume (OBV)

pvi --> Positive Volume Index (PVI)

dvdi --> Dual Volume Divergence Index (DVDI)

xhh --> Dynamic rolling highest values

pvt --> Price-Volume Trend (PVT)

Remarks

I also incorporated func descriptions and func test script in commented mode, you can test the functino with the embedded test script and modify them as you wish.

This is a Level 3 free and open source indicator library.

Feedbacks are appreciated.

This is not the end of pandas_ta lib publication, but it is start point with pine v5 lib function and I will add more and more funcs into this lib for my own indicators.

Function Name List:

bton()

wcp()

count()

xbt()

ebsw()

ao()

apo()

xrf()

bias()

bop()

brar()

cci()

cfo()

cg()

cmo()

coppock()

cti()

dmi()

er()

eri()

fisher()

inertia()

kdj()

kst()

macd()

mom()

pgo()

ppo()

psl()

pvo()

qqe()

roc()

rsi()

rsx()

rvgi()

slope()

smi()

sqz_pro()

xfl()

stc()

stoch()

stochrsi()

trix()

tsi()

uo()

willr()

alma()

wcx()

xll()

dema()

ema()

fwma()

hilo()

hma()

hwma()

ichimoku()

jma()

kama()

linreg()

mgcd()

rma()

sinwma()

ssf()

supertrend()

xsa()

swma()

t3()

tema()

trima()

vidya()

vwap()

vwma()

wma()

zlma()

entropy()

kurtosis()

skew()

xev()

zscore()

adx()

aroon()

chop()

xex()

cksp()

dpo()

long_run()

psar()

short_run()

vhf()

vortex()

accbands()

atr()

bbands()

donchian()

kc()

massi()

natr()

pdist()

rvi()

thermo()

ui()

ad()

cmf()

efi()

ecm()

kvo()

mfi()

nvi()

obv()

pvi()

dvdi()

xhh()

pvt()

Combo Backtest 123 Reversal & Relative Momentum Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Relative Momentum Index (RMI) was developed by Roger Altman. Impressed

with the Relative Strength Index's sensitivity to the number of look-back

periods, yet frustrated with it's inconsistent oscillation between defined

overbought and oversold levels, Mr. Altman added a momentum component to the RSI.

As mentioned, the RMI is a variation of the RSI indicator. Instead of counting

up and down days from close to close as the RSI does, the RMI counts up and down

days from the close relative to the close x-days ago where x is not necessarily

1 as required by the RSI). So as the name of the indicator reflects, "momentum" is

substituted for "strength".

WARNING:

- For purpose educate only

- This script to change bars colors.

Market Strength ScannerHey traders, this is a table-based market relative strength and true strength scanner, designed to allow the users to get data from multiple pairs without having to go onto that pair for their strength's. This indicator uses functions to fetch data from other pairs so that the code is optimised and prevents slow loading. Furthermore, the indicator is easy to understand and use as there isn't a lot of settings for it, you can adjust the length of the true strength index or the relative strength index through one input box, you can change the data type from RSI to TSI without changing the code, and you can customise what pairs you want to display. Furthermore, the user can set alerts for the pairs that they want to have such as setting alerts for overbought and oversold zones. That's all to this indicator and I hope it is of use to some people :)

RelativeStrengthComparative_IBD_YRKI am publising Relative Strength Comparative.

It is be used to compare a Stock's Performance against another stock/index (Default NIFTY50)

I also devised a Plot RS Rating which is inspired from IBD's RS Rating and matches to some extent. You can turn off/on the RS Rating as per need.

Example: ITC vs NIFTY 50 it will be ITC / NIFTY

The Indicator can be used in Multiple ways:

1) Check Relative Strength

2) Check RS Rating (This is not Accurate as of now since IBD compares the ratings of all the stocks in an Exchange)

3) Can be used as a Spread Chart for the Division (We need to not divide every time we change Stocks)

4) Design a Template exactly as MarketSmith by using the TradingView feature of "Move to --> Existing Pane Above"

The Formula i used for RS Rating is below with more weightage on the 3 month performance and lesser on 12 month Performance. I am open to Modification of this Formula if a better suggestion

// relative strength IBD style

ThreeMthRS = 0.4*(close/close)

SixMthRS = 0.2*(close/(close*2))

NineMthRS = 0.2*(close/(close*3))

TwelveMthRS = 0.2*(close/(close*4))

(JS) Ultimate RSISo my goal here was to combine all of my RSI ideas into a single indicator in order to make kind of a "Swiss Army Knife" version of the Relative Strength Index ...

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

So, let's begin with the first RSI indicator I made, which is the RSIDVW (Divergence/Volume Weighted);

To rephrase my original post, the "divergence/volume weighted" portion is meant to expand upon the current RSI format by adding more variables into the equation.

The standard RSI is based off one value that you select (open, close, OHLC4, HLC3, etc.) while this version takes three variables into account.

The default setting is to have RSI normal without anything added to it (Divergence Weight = 0)

1st - it takes the standard variable that RSI normally uses.

2nd - it factors RSI divergence by taking the RSI change % and price change % to form a ratio. Using this ratio, I duplicated the RSI formula and created a divergence RS to be factored in with the standard price RS .

3rd - it takes Relative Volume and amplifies/weakens the move based upon volume confirmation. (So if Relative Volume for a price bar is 1.0, the RSI plot would be the same as it normally would)

So to explain the parameters

- Relative Volume Length: This uses the RV length you specify to determine spikes in volume (or lack of volume ), which then is added into the formula to influence the strength of the RSI move

- RV x Divergence: This is how I calculated the original formula, but you can leave this unchecked to turn Relative Volume off, or apply elsewhere.

- RV x RS: There's two sides, Divergence RS and Standard RS - these check marks allow you to select which part you prefer to be multiplied by Relative Volume .

Checking neither turns off Relative Volume , while checking both amplifies its effects by placing it on both sides of the equation.

-Divergence Weight: This controls how much the DVW portion of the formula influences the RSI plot. As I referred to earlier, default is 0 making RSI normal. The Scale is 0-2, so 1.0 would be the same as 50%.

When I do have DVW on, I generally set it to 0.5

-SMA Divergence: To smooth, or not to smooth, that is the question. UJsing an SMA here is much smoother in my opinon, but leaving it unchecked runs it through an RMA the same way standard RSI is calculated.

-Show Fractal Channel: This allows you to see the whole fractal channel around the RSI (This portion of the code, compliments of the original Ricardo Santos fractal script)

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

The next portion of the script is adding a "Slow RSI"...

This is rather simple really, it allows you to add a second RSI plot so that you can watch for crossovers between fast and slow lines.

-Slow RSI: This turns on the second RSI Plot.

-Slow RSI Length: This determines the length of the second RSI Plot.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Pivot Point RSI was something a friend of mine requested I make which turned out pretty cool, I thought... It is also available in this indicator.

-Pivot Points: Selecting this enables the rest of the pivot point related parts of the script

If Pivot Points isn't selected, none of the following things will work

-Plot Pivot: Plots the pivot point .

-Plot S1/R1: Plots S1/R1.

-Plot S2/R2: Plots S2/R2.

-Plot S3/R3: Plots S3/R3.

-Plot S4/R4: Plots S4/R4.

-Plot S5/R5: Plots S5/R5.

-Plot Halfway Points: Plots a line between each pivot .

-Show Pivot Labels: Shows the proper label for each pivot .

When using intraday charts, from a 15 minute interval or less the pivots are calculated based on a single days worth of price action, above that the distance expands.

Here are the current resolutions Pivot Points will work with:

Minutes - 1 , 2, 3, 5, 10, 13, 15, 20, 30, 39, 78, 130, 195

Hours - 1, 2, 3, 4, 5, 6

Daily

Weekly

Currently not available on seconds or monthly

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Background Colors

Background Colors: I have six color schemes I created for this which can be toggled here (they can be edited).

Gray Background for Dark Mode: Having this on looks much better when using dark mode on your charts.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Now finally the last portion, Fibonacci Levels

-Fibonacci Levels: This is off, by default, which then uses the standard levels on RSI (30-50-70). When turned on, it removes these and marks fib levels from 0.146 through 0.886.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

So the quick rundown:

Ultimate RSI contains "divergence/volume weighted" modifications, a slow RSI plot, pivot points , and Fibonacci levels all while auto-plotting divergence and having the trend illustrated in the background colors.

RSI has always been my "go to" indicator, so I hope you all enjoy this as much as I do!

Rumpy's Dynamic Momentum IndexNote : I haven't been able to determine from the info I've found whether the variable length is used for the average gain/loss part of the calculation and/or for the relative strength portion of the calculation . If anyone knows for certain please let me know.

Type A only uses the variable length for the final relative strength calculation and the fixed RSI length for the average gain/loss.

Type B uses the variable length for both.

I do suspect that Type B is correct though as it is a lot more sensitive to momentum changes while Type A tends to just exaggerate normal RSI

-------------------------------------------------------------------------------------------------------------------------------------------

This indicator, developed by Tushar Chande and Stanley Kroll, is similar to the relative strength index (RSI). The main difference between the two is that the RSI uses a fixed number of time periods (usually 14) in its calculation, while the dynamic momentum index uses different time periods as volatility changes, typically between five and 30.

The dynamic momentum index uses fewer periods in its calculation when volatility is high, and more periods when volatility is low.

The number of time periods used in the dynamic momentum index decreases as volatility in the underlying security increases, making this indicator more responsive to changing prices than the RSI. This is particularly useful when an asset's price moves quickly as it approaches key support or resistance levels. Because the indicator is more sensitive, traders can potentially find earlier entry and exit points than with the RSI.

-------------------------------------------------------------------------------------------------------------------------------------------

If you find it useful please consider a tip/donation :

BTC - 3BMEXEDyWJ58eXUEALYPadbn1wwWKmf6sA

[ALERTS] ADX and DIThe average directional index (ADX) is a technical analysis metric. Analysts use it to determine the relative strength of a trend, with the direction of the trend either upwards or downwards.

The Average Directional Index (ADX) along with the Negative Directional Indicator (-DI) and the Positive Directional Indicator (+DI) are momentum strength indicators that evolved for use in stock trading. Commodities trader J. Welles Wilder pioneered their use. Technical traders who use charting techniques want to know when first spotting a shifting trend how strong that trend is and how likely it is to sustain itself over time. The ADX helps investors determine trend strength as they plan their investment strategies.

Confirmation on a chart and other momentum indicators help investors spot trend reversals. But some trends are more potent than others and investors want to better understand the strength of a trend. The ADX identifies a strong positive trend when the ADX is over 25 and a weak trend when the ADX is below 20. Investors can determine directional movement by analyzing the difference between two consecutive low prices and their correlated highs. The movement is +DM when the current high price, less the previous high price, is greater than the previous low price less the current low. The opposite applies in determining the negative or –DI.

When analyzing charts, stock price is the single most important variable to follow. ADX and other indicators are supplementary to price movements in providing additional directional information and support. For example, some of the best trends come about from price range consolidation. It is those tugs of war between buying and selling volumes that lead to breakouts and other trading opportunities.

The Inventor of the Average Directional Index

J. Welles Wilder, Jr. is a former American engineer and real estate developer who went on to revolutionize trading analysis by applying mathematical systems to the world of investing. In addition to developing the ADX, Wilder is also responsible for several other commonly used technical analysis tools including the Average True Range (ATR), the Relative Strength Index (RSI) and the Parabolic SAR.

www.investopedia.com

This script has alerts and includes the filter for markets with no trend defined.

Green Alert --> Long

Red Alert --> Short

Yellow Area --> Weak trend. ADX below threshold

Green candles --> Bullish Market

Red Candles --> Bearish Market

Orange candles --> No defined trend

Enjoy!

Relative Momentum Index Backtest The Relative Momentum Index (RMI) was developed by Roger Altman. Impressed

with the Relative Strength Index's sensitivity to the number of look-back

periods, yet frustrated with it's inconsistent oscillation between defined

overbought and oversold levels, Mr. Altman added a momentum component to the RSI.

As mentioned, the RMI is a variation of the RSI indicator. Instead of counting

up and down days from close to close as the RSI does, the RMI counts up and down

days from the close relative to the close x-days ago where x is not necessarily

1 as required by the RSI). So as the name of the indicator reflects, "momentum" is

substituted for "strength".

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Relative Momentum Index Strategy The Relative Momentum Index (RMI) was developed by Roger Altman. Impressed

with the Relative Strength Index's sensitivity to the number of look-back

periods, yet frustrated with it's inconsistent oscillation between defined

overbought and oversold levels, Mr. Altman added a momentum component to the RSI.

As mentioned, the RMI is a variation of the RSI indicator. Instead of counting

up and down days from close to close as the RSI does, the RMI counts up and down

days from the close relative to the close x-days ago where x is not necessarily

1 as required by the RSI). So as the name of the indicator reflects, "momentum" is

substituted for "strength".

WARNING:

- This script to change bars colors.

Currency Relative Strengths V.2 [GM]Version 2 Updates

Speed has been increased by ~7X

Highest and lowest pairs now highlighted using brighter colors

Re-ordered pairs from highest to lowest 'flight to risk' rating

I created this tool for the purpose of determining strongest and weakest currencies over different periods of time. Each major currency is compared to the field of other majors and its average change is measured over a predetermined period of time. The result is displayed as a percentage. I use it for trend following but it can also be used to fade exhaustion.

Instructions

Add indicator to chart

Select a time frame under settings

Place cursor over period of interest

Click "Data Window" on right hand side bar

View % change avg values for each currency

Relative Momentum Index The Relative Momentum Index (RMI) was developed by Roger Altman. Impressed

with the Relative Strength Index's sensitivity to the number of look-back

periods, yet frustrated with it's inconsistent oscillation between defined

overbought and oversold levels, Mr. Altman added a momentum component to the RSI.

As mentioned, the RMI is a variation of the RSI indicator. Instead of counting

up and down days from close to close as the RSI does, the RMI counts up and down

days from the close relative to the close x-days ago where x is not necessarily

1 as required by the RSI). So as the name of the indicator reflects, "momentum" is

substituted for "strength".

IKZ MAX# 📊 RSI + Volume Profile Integrated Indicator

## 🎯 **General Description**

An integrated indicator that combines the power of **RSI (Relative Strength Index)** and **Volume Profile** in one technical analysis tool. It blends momentum analysis with volume distribution to provide more accurate and reliable trading signals.

## 📈 **Main Components**

### 1. **RSI (Relative Strength Index)**

- **Function**: Measures the speed and magnitude of price changes

- **Levels**:

- 🟥 **Overbought (70)**: Potential selling area

- 🟩 **Oversold (30)**: Potential buying area

- ⚪ **Midline (50)**: Balance line

### 2. **Volume Profile**

- **Function**: Analyzes trading volume distribution across price levels

- **Components**:

- 🟡 **POC (Point of Control)**: Price level with highest trading volume

- 🔵 **Value Area**: Area containing 68% of trading volume around POC

## ⚡ **Trading Signals**

### 📊 **Traditional RSI Signals**

- 🟢 **RSI Buy Signal**: When RSI crosses above 30 level (oversold)

- 🔴 **RSI Sell Signal**: When RSI crosses below 70 level (overbought)

### 💪 **Strong Integrated Signals**

- 💚 **Strong Buy**: RSI in oversold + Price near POC

- 🖤 **Strong Sell**: RSI in overbought + Price near POC

## 🛠 **Adjustable Settings**

### ⚙️ **RSI Settings**

- `rsi_length`: Calculation period (default: 14)

- `rsi_overbought`: Overbought level (default: 70)

- `rsi_oversold`: Oversold level (default: 30)

- `rsi_src`: Data source (default: close price)

### 📊 **Volume Profile Settings**

- `vp_lookback`: Lookback period (number of candles)

- `vp_rows`: Number of rows (distribution precision)

- `show_vp_histogram`: Show volume histogram

- `show_poc`: Show Point of Control

- `show_value_area`: Show Value Area

## 🎨 **Visual Elements**

### 📉 **Chart Display**

- RSI line in blue color

- Colored areas for extremes (red/green)

- POC line with label

- Buy/sell signals as colored triangles

### 📋 **Information Table**

- Current RSI value and status

- Current POC price

- Value Area range

- Current active signal

- Current active volume

## 🔔 **Alert Systems**

- Alerts for traditional RSI signals

- Alerts for integrated strong signals

- Updates once per bar

## 💡 **Trading Applications**

### 1. **Support and Resistance Identification**

- POC forms strongest support/resistance levels

- Value Area defines main trading range

### 2. **Momentum and Trend Analysis**

- RSI determines current momentum strength

- Volume Profile confirms level strength

### 3. **Entry Timing**

- Enter when integrated signals converge

- Confirm momentum alignment with volume distribution

## 🚀 **Unique Features**

### ✅ **Smart Integration**

- Combines two powerful indicators in one interface

- Integrated signals provide stronger confirmation

### ✅ **Flexibility**

- Fully customizable settings

- Suitable for all timeframes

### ✅ **User-Friendly**

- Clear visual interface

- Direct and easy-to-read signals

## 📊 **Result Interpretation**

### 🟢 **Ideal Buy Scenario**

- RSI below 40 (potential upward momentum)

- Price near POC (strong support)

- Buy signal from both indicators

### 🔴 **Ideal Sell Scenario**

- RSI above 60 (potential downward momentum)

- Price near POC (strong resistance)

- Sell signal from both indicators

## ⚠️ **Important Notes**

### 🔧 For Daily Timeframe:

- `vp_lookback = 50` (lookback period)

- `rsi_length = 14` (RSI period)

### 🔧 For Hourly Timeframe:

- `vp_lookback = 100` (lookback period)

- `rsi_length = 14` (RSI period)

## 📝 **Usage Tips**

1. **Strong Signals**: Wait for confirmation from both indicators before entering trades

2. **Risk Management**: Use POC as support/resistance for stop-loss placement

3. **Timing**: Best signals occur when RSI crosses critical levels with Volume Profile confirmation

## ⚠️ **Warning**

This indicator is for educational and analytical purposes only, not financial advice. Always practice risk management and never trade more than you can afford to lose.

---

**📈 Enjoy Smart Trading!** 🚀

neeson macd-volNeeson MACD-Vol Indicator - Feature Description & User Manual

📊 Indicator Overview

Neeson MACD-Vol is a comprehensive technical analysis indicator that combines MACD, volume, RSI, ATR, and OBV to provide traders with a complete market analysis perspective.

⚙️ Core Features

1. Smooth MACD Analysis

MACD Line Smoothing Filter: Supports three smoothing methods: EMA, SMA, WMA

Crossover Signal Confirmation: Uses closing price to confirm golden/death crosses, avoiding false signals

Signal Filtering Mechanism: Filters frequent false signals based on time and strength criteria

2. Volume Analysis

Extreme Volume Detection: Identifies abnormal high volume and highlights with white histogram bars

Volume Ratio Display: Real-time display of current volume relative to moving average

VOL Labels: Shows volume ratio labels at extreme volume positions

3. Multi-dimensional Divergence Detection

Price-Volume Divergence: Identifies divergence between price and volume

Price-RSI Divergence: Detects momentum divergence for early trend reversal signals

Price-OBV Divergence: Analyzes divergence between money flow and price action

4. Auxiliary Indicators

RSI Indicator: Displays Relative Strength Index with overbought/oversold zones

ATR Indicator: Measures market volatility and identifies high/low volatility periods

OBV Indicator: On-Balance Volume for analyzing money flow and accumulation

🎯 Usage Instructions

Trade Signal Identification

Buy Signals:

🟢 MACD Golden Cross (Orange dots)

🟢 Bullish Volume Divergence (Green triangles)

🟢 Bullish RSI Divergence (Cyan "RSI" labels)

🟢 Bullish OBV Divergence (Cyan "OBV" labels)

⚪ Extreme Buy Volume (White histogram bars)

Sell Signals:

🔵 MACD Death Cross (Blue dots)

🔴 Bearish Volume Divergence (Red triangles)

🔴 Bearish RSI Divergence (Magenta "RSI" labels)

🔴 Bearish OBV Divergence (Magenta "OBV" labels)

⚪ Extreme Sell Volume (White histogram bars)

Parameter Configuration

MACD Parameters:

Fast Length (Default: 12)

Slow Length (Default: 26)

Signal Length (Default: 9)

Volume Parameters:

Extreme Volume Threshold (Default: 2.5x)

Divergence Lookback Period (Default: 20)

Filtering Parameters:

Minimum Bars Between Signals (Default: 5 bars)

Minimum MACD Strength (Default: 0.001)

⚠️ Risk Disclaimer

English Version:

This indicator is for technical analysis reference only and does not constitute any investment advice. Financial market trading involves high risks and may lead to capital loss. Past performance is not indicative of future results. Users should fully understand the relevant risks, conduct their own research, and consult with qualified financial advisors before making any investment decisions. The user assumes full responsibility for their trading decisions and any resulting losses. The author is not responsible for any direct or indirect losses, financial or otherwise, caused by using this indicator.

📄 Copyright Notice

Copyright © 2024 Neeson1987

X/Twitter: @neeson1987

All intellectual property rights for this indicator are owned by Neeson1987. This includes but is not limited to the source code, algorithm, visual design, and documentation. No part of this indicator may be copied, reproduced, modified, distributed, sold, or used for commercial purposes without explicit written permission from the author. Personal use is permitted.

Unauthorized reproduction or distribution of this indicator may result in legal action. For licensing inquiries or commercial use, please contact via X/Twitter: @neeson1987.

🔍 Usage Recommendations

Multiple Confirmations: Combine multiple signals for trading decisions

Timeframe Analysis: Verify signal consistency across different timeframes

Risk Management: Always use stop-loss and proper position sizing

Market Context: Consider current market volatility and trend conditions

Continuous Learning: Regularly update parameters and adapt to market changes

Paper Trading: Test strategies in demo accounts before live trading

Journaling: Keep records of trades and indicator performance

🔧 Technical Specifications

Platform: TradingView Pine Script v5

Compatibility: Stocks, Forex, Crypto, Futures, and other financial instruments

Timeframes: All timeframes supported

Update Frequency: Real-time calculation

📞 Support & Updates

For technical support, bug reports, or update notifications:

X/Twitter: @neeson1987

Update Channel: Follow X account for latest versions

📈 Happy Trading! | May the trends be with you!

Note: This indicator is continuously improved. Always ensure you're using the latest version for optimal performance.

Holt Damped Forecast [CHE]A Friendly Note on These Pine Script Scripts

Hey there! Just wanted to share a quick, heartfelt heads-up: All these Pine Script examples come straight from my own self-study adventures as a total autodidact—think late nights tinkering and learning on my own. They're purely for educational vibes, helping me (and hopefully you!) get the hang of Pine Script basics, cool indicators, and building simple strategies.

That said, please know this isn't any kind of financial advice, investment nudge, or pro-level trading blueprint. I'd love for you to dive in with your own research, run those backtests like a champ, and maybe bounce ideas off a qualified expert before trying anything in a real trading setup. No guarantees here on performance or spot-on accuracy—trading's got its risks, and those are totally on each of us.

Let's keep it fun and educational—happy coding! 😊

Holt Damped Forecast — Damped trend forecasts with fan bands for uncertainty visualization and momentum integration

Summary

This indicator applies damped exponential smoothing to generate forward price forecasts, displaying them as probabilistic fan bands to highlight potential ranges rather than point estimates. It incorporates residual-based uncertainty to make projections more reliable in varying market conditions, reducing overconfidence in strong trends. Momentum from the trend component is shown in an optional label alongside signals, aiding quick assessment of direction and strength without relying on lagging oscillators.

Motivation: Why this design?

Standard exponential smoothing often extrapolates trends indefinitely, leading to unrealistic forecasts during mean reversion or weakening momentum. This design uses damping to gradually flatten long-term projections, better suiting real markets where trends fade. It addresses the need for visual uncertainty in forecasts, helping traders avoid entries based on overly optimistic point predictions.

What’s different vs. standard approaches?

- Reference baseline: Diverges from basic Holt's linear exponential smoothing, which assumes persistent trends without decay.

- Architecture differences:

- Adds damping to the trend extrapolation for finite-horizon realism.

- Builds fan bands from historical residuals for probabilistic ranges at multiple confidence levels.

- Integrates a dynamic label combining forecast details, scaled momentum, and directional signals.

- Applies tail background coloring to recent bars based on forecast direction for immediate visual cues.

- Practical effect: Charts show converging forecast bands over time, emphasizing shorter horizons where accuracy is higher. This visibly tempers aggressive projections in trends, making it easier to spot when uncertainty widens, which signals potential reversals or consolidation.

How it works (technical)

The indicator maintains two persistent components: a level tracking the current price baseline and a trend capturing directional slope. On each bar, the level updates by blending the current source price with a one-step-ahead expectation from the prior level and damped trend. The trend then adjusts by weighting the change in level against the prior damped trend. Forecasts extend this forward over a user-defined number of steps, with damping ensuring the trend influence diminishes over distance.